There has been a historic shift in how we live, work, and do business. Consumers and merchants across all ages, demographics, and industries have become more comfortable with a digital way of living and doing business, and this includes making digital payments. Fintech companies have led the charge with a variety of solutions that deliver frictionless, transparent, and faster payment solutions that make paying easy. From ordering groceries to buying a car to settling a split dinner bill with friends, most experiences, goods, and transactions can be handled at the touch of a button.

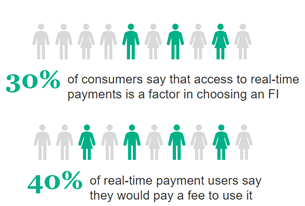

As our economy becomes increasingly digitized, consumers and businesses are expecting payments to be not just faster but immediate. As a result, the financial services industry is at a tipping point, with immediate payments in a prime position to be utilized as the primary digital payment solution of the future. Supported by two new payment rails, (The Clearing House’s RTP® network and the Federal Reserve’s future FedNowSM Service), immediate payments are here. In fact, real-time payments are already affecting consumers’ choice of financial institution, with one third of consumers saying that access to real-time payments is a factor in their choice (Pymnts.com, Dec. 2021). Additionally, nine out of 10 business expect to make faster payments, including instant payments, by 2023 (2020 Federal Reserve Study).

Source: PYMNTS.com Real-Time Payments Tracker, December 2021

As the rapid evolution of the payments ecosystem continues, we must recognize that it’s critical to begin adopting real-time payments as soon as possible. Understanding the essential elements of real-time payments—what they are and what they are not—will establish a solid foundation from which your credit union can get started.

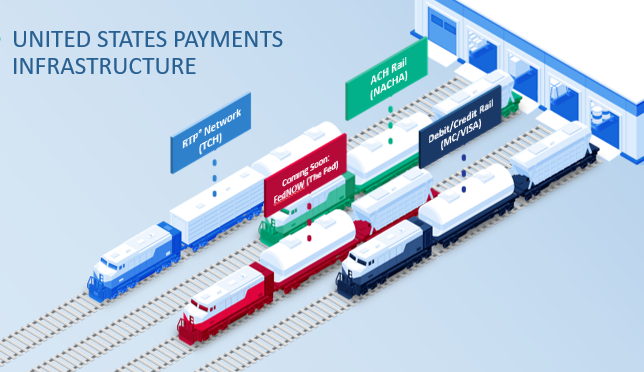

Identifying the transaction rails

In today’s payment world, transactions travel on separate rails. There’s the ACH rail, the debit/credit rail, and, most recently, The Clearing House’s RTP network, which has been live since 2017. The RTP network facilitates real-time payments and is not part of the other payment rails. The Federal Reserve is also planning to launch its own instant payment rail in 2023 called the FedNow Service.

Like ACH, both rails support separate participant profiles for Receive Only, Send/Receive and others. Many credit unions will find getting started with real-time payments as receive only is the best way to dip their toes into the water and enable their members to receive real-time payments, and we agree. This is a smart strategy. It requires the lightest lift and the least risk. Like with ACH, credit unions will be able to evolve their profile over time and as it aligns with their payments strategy.

Financial institutions must connect and be a participant of some level on either RTP or FedNow (when it launches) or both to receive and/or send immediate payments. At this time, RTP and the FedNow Service will operate separately, and financial institutions will need to connect to, and at least receive transactions, on both rails to remain competitive.

Understanding faster payments vs. real-time payments

Though sometimes the terms “faster payments” and “real-time (and/or immediate) payments” are used interchangeably, they really are two different things. Real-time payments stand apart from other legacy payment systems in five substantial ways:

- Real-time payments are certified. The payment authenticity is guaranteed.

- Real-time payments are final. They cannot be revoked or recalled once authorized by a sender and submitted. There is a Request for Return of Funds if real-time payment funds are sent in error, but this process takes place after settlement. In comparison, any returns on legacy payment systems can take place before funds are settled.

- Real-time payments are immediately available to the receiver. Senders and recipients also receive a status notification that funds were sent and that they are now available. Legacy payment systems clear in batches at varying times. Senders may not know for a few days if a transfer was successful and that funds are available to the receiver to use.

- Real-time payments are instantly settled. Legacy payments are settled by batch and at varying time intervals; with real-time payments, financial institutions settle funds instantly and individually.

- Real-time payments are confirmed. The payee and payor receive notifications of payment status. Legacy systems typically only provide the payer with a notification that the payment was sent.

Debunking misconceptions about real-time payments

Payments made through Zelle, PayPal or Venmo are not real-time payments. Zelle, PayPal and Venmo are the only front-end applications that allow consumers to initiate a payment via an ACH, a debit, or the RTP network rail.

In addition, signing up for Zelle does not give your credit union access to the RTP network. To transact payments on this rail, your credit union must be a participant and connect to the RTP network to receive or send funds via a front-end application for RTP. Just as you need to be an ODFI or RDFI on ACH to process ACH payments, you need will need to be a participant on the RTP network to receive/send real-time payments.

Managing risk and fraud

Real-time payments relieve a lot of the settlement risk that financial institutions face today. Settlement risk is very real in existing payment forms, but by using a credit-push (good funds) model, which verifies money is available before it is sent, the real-time payments model eliminates transaction settlement risk on their network. Though this model doesn’t mitigate fraud, it does eliminate settlement risk.

This means, for those financial institutions that start with receive only, there is no risk because the credit-push model verifies the funds are good when they are sent. Starting your real-time payments journey as a “receive-only” participant will allow your financial institution to enable access to RTP or the FedNow Service for your members without bearing the transactional risk. You can apply risk/exposure mitigation tools that each new rail offers (such as setting send- and time-of-day limits) and extend existing fraud prevention methods to the rail you’re on as you migrate to a send profile.

Benefitting from real-time payments

Real-time payments offer numerous benefits to credit unions and the members they serve. Below are some examples of key benefits that often resonate most with financial institutions:

- Grow revenue by supporting a variety of use cases. Recent industry research reports that 40% of RTP users would willingly pay fees to get their payments in real time, and 2 in 3 consumers say they would be more likely to continue doing business with firms that provide a real-time payment option. Further, approximately 50% of insurance, income and earning disbursement recipients would be willing to pay a fee to receive those payments instantly.

- Remain competitive by fulfilling members’ expectations and desire for instant payments. Real-time payments are growing significantly while traditional check and cash continue to decline. In 2021, real-time payments tripled. Research says more than 1/3 of U.S. consumers cite access to real-time payments as a factor in choosing their financial institution. The RTP rail currently reaches more than 60% of U.S. demand deposit accounts.

- Address gaps in current payment methods through additional data, requests, security, and immediate availability. Real-time payments can facilitate a new request for payment (RfP), which allows a business or a consumer to send a request in the form of a message and provides the payor with the option to authorize or deny the payment. Push, or credit, transactions enable payers to instruct their financial institution to send money from their accounts to recipients’ accounts, putting the payer in control of the timing of the release of their funds. The contextual data surrounding a payment has been missing from every previous payment system. Using the ISO2022 financial messaging methodology that creates standard, consistent payment messages across all business processes within the financial services industry, real-time payments offer the ability to attach information about the payment that doesn’t detach throughout the process, which is helpful during payment processing and reconciliation. Real-time payments facilitate real-time authorization, real-time posting, and real-time clearing and settlement.

Reimagining your business with real-world use cases

When most people think about real-time payments, the first use case that comes to mind is person-to-person payments. But as you can see with the following graphic from The Clearing House, ways you can use real-time payments are as diverse as the credit unions.

This chart is not an all-inclusive list of every type of use case, either. The ways to use real-time payments are almost limitless. As each credit union experiments with and experiences immediate payments and analyzes their payment data, they will learn what use cases are most valuable to their specific credit union. And that’s the greatest benefit of this new payment option—the tremendous opportunity to enhance how credit unions serve members, streamline credit union business functions, and generate new products and revenue.

Exploring the next steps in your RTP journey

Whether you’re just getting started or already considering real-time payments for your credit union, Corporate One can help. Schedule an RTP Discovery Meeting and we can focus on one of the following:

- Providing education: Learn more about real-time payments specifics and why now is the right time for your credit union to consider real-time payments.

- Providing strategic direction: As a certified RTP participant and solution provider, we can guide your credit union on the key decision points it needs to make to get started on the RTP network.