I often hear two questions when talking with credit unions about immediate payments: "What network do I choose? And what do I really need to do to get started?” Though immediate payments offer exciting new opportunities for credit unions to modernize their offerings and grow membership and revenue, there’s no “easy” button for implementing/connecting the industry’s two new immediate payment rails—the RTP® network and the FedNow® Service.

RTP vs FedNow: What To Consider

Fortunately, we at Corporate One have done a lot of the groundwork for you regarding understanding what decisions are necessary and what is needed to get the ball rolling. There are two main things to consider when choosing an immediate payments rail:

- Interoperability

- Reach and member needs

Interoperability. Unfortunately, the RTP network and the FedNow service will not be interoperable, at least for the foreseeable future. The new immediate payment rails are unlike ACH (having access to one ACH provider gives you access to all ACH providers). The result will be that some financial institutions will choose the RTP network, and some will prefer the FedNow service. This means that if your member is sent money via the RTP network but you only use the FedNow Service, your member will be unable to receive their funds. So, the answer to the interoperability consideration is to choose both rails. At the very least, you’ll need to be able to at least receive on both immediate payment rails.

Reach and member needs. Once your credit union is comfortable receiving funds on the RTP network and FedNow Service, the next step is eventually to expand from a Receive profile to a Send profile. Consider whom you are trying to reach and what is the demand from your members. Credit unions must determine which use cases (such as P2P, C2B, B2C, B2B, A2A, etc.) they will facilitate and the specific payment rail they will focus on to develop a Send experience for their members on that rail. Which use cases provide the most significant benefits for your credit union? And which payment rail offers the most extensive coverage to maximize those benefits? Helpful insight will be gained if you can understand your members' needs/expectations, marketplace demands, and the problems your credit union is trying to solve. To develop a broader understanding overall, it may also be helpful to reach out to your local payments association or credit union peers in your area to hear what other professionals are doing and other memberships are saying.

RTP Network and FedNow Service: Differences in Functionality

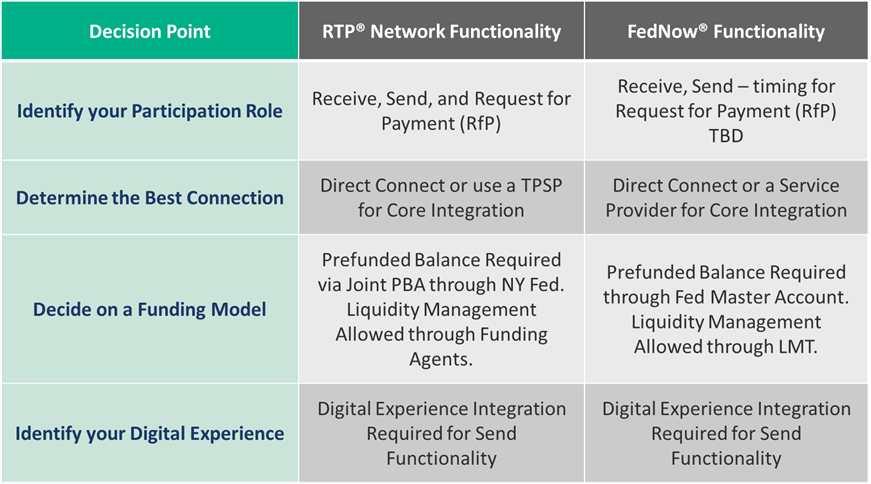

Once you’ve considered these points and decided on which rail to implement first, you’ll need to make four main decisions, as visualized in the following chart:

RTP Network and FedNow Service Decision Points Explained

As you can see, the RTP network and FedNow Service are structured very similarly. So, regardless of your choice, your credit union will still face four decision points as you move along your journey. Below is a summary of each decision point:

- Identify your participation role. Both the FedNow Service and RTP network rails provide the ability to receive, send, and a request for payment (RfP) profile. At the very least, credit unions need to move toward the ability to receive on a rail.

- Determine the best connection: Immediate payments require a connection to a core, so one of the most important decisions is analyzing the best method to connect your core to one of the rails. This connection can be achieved directly or through a third-party service provider. (On the RTP network, this is defined as just a “Service Provider.”)

- Decide on a funding model. The RTP network and FedNow Service require send-participant credit unions to have a prefunded balance, and both rails allow for liquidity management. On the RTP network, this is done through a Funding Agent. On the FedNow Service, this is accomplished using the liquidity management tool. While receive-participant credit unions will not be concerned with prefunding monies, we encourage credit unions to decide on a funding model at the outset because making this choice during initial onboarding will allow you to evolve more seamlessly to a send profile later.

- Identify your digital “experience.” Because a connection to a payments rail is just a connection (no front-end experience included), each credit union will need to develop and integrate a way for your membership to use your new immediate payments service. For receive-only participants, an experience isn’t required. But if your credit union wants to enable businesses or members to send payments, you will need a front-end experience to do so. And there are several front-end experiences out in the marketplace that you are already probably familiar with. Most of the RTP network’s volume today flows through digital wallet experiences like Venmo, PayPal, Coinbase, Robinhood, and Square.

To begin understanding what type of front-end experience your credit union needs, you'll need to understand what use cases would be most beneficial to your credit union. For example, do you need an experience for P2P or A2A? Are your business members asking to use RfP for their billing? For an extensive “at-a-glance" list of use cases, our RTP Use Cases Infographic is a helpful resource.

For more information, visit our Real-Time Payments Info Center and I encourage you to contact me at 866/MyCorp1 or via [email protected] to discuss the next steps in your immediate payments journey.

Toby Thomas

VP, Product Market Strategist

Keep up to date with our quarterly newsletter the Immediate Payments Insider.